As a financial/business/valuation analyst, many times we have to spend a considerable amount of time trying to find the VALUE of companies.

There are many different aspects of value – different terms get used synonymously and often causes a lot of confusion.

We thought we will help to end the confusion between the different terminologies that exist out there.

This will help you in having a meaningful discussion with your clients and colleagues and help to focus on the right metric when trying to value a company.

Lets go straight into it.

Enterprise value:

This is the one of the most relevant aspect of value of a company and something that is least understood by many.

Let us help you explain this with an example.

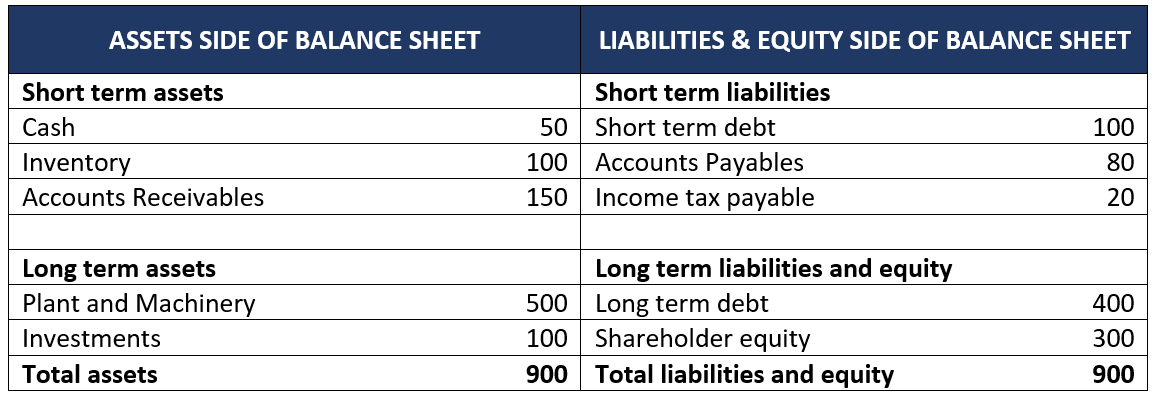

Now, you would all have seen a balance sheet of any company.

Typically, it looks like below:

The assets and liabilities that you see above constitute the overall business of the Firm.

However, not all line items are used in the operations of the business.

Some of the line items are OPERATIONAL and some are FINANCIAL in nature.

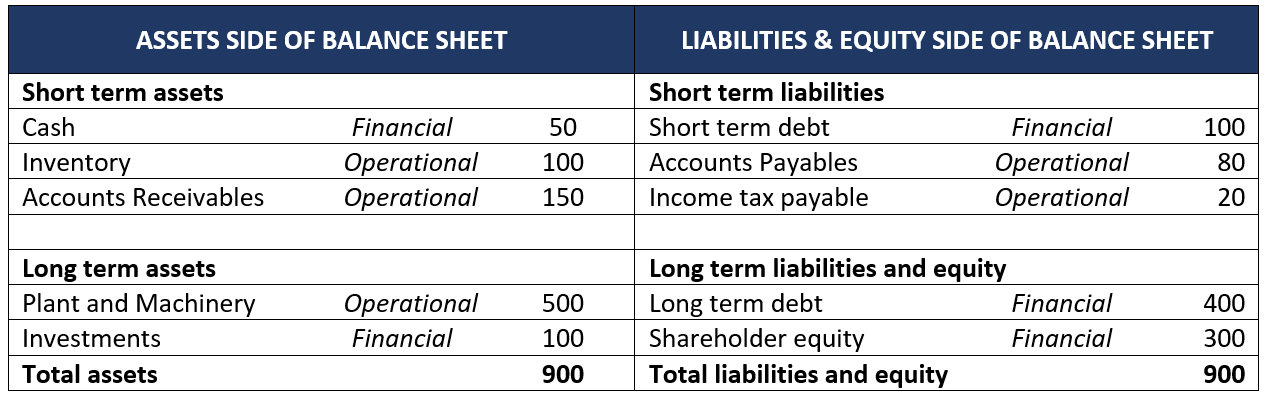

Operating items are those that get used in the day to day business of the Firm.

On the Assets side, items like – Inventory, Accounts Receivables and Plant and machinery are purely OPERATIONAL in nature.

Similarly, on the Liabilities side, items like – Accounts Payables and Income tax payable are also OPERTIONAL in nature.

The remaining line items are purely FINANCIAL in nature in the sense that they either finance the business or are invested outside the core business.

So Cash and Investments reflect surplus funds not directly used in the business. Hence, they are more of a FINANCIAL transaction.

Similarly, Short-term debt and Long-term debt reflect the external financing the firm has received for running the business. It is also FINANCIAL in nature.

Shareholder equity is also FINANCIAL in nature as it reflects the capital provided by the owners of the business for financing the business.

So if we were to re-classify the Balance Sheet into OPERATIONAL AND FINANCIAL items, it would look something like below:

Now, lets say somebody asked what is the total operational value of the Firm.

We can simply add all the operational assets and subtract the operational liabilities.

In this case, it will be

Inventory + A/Receivables + Plant and Machinery – A/Payables – IT payable

= 100 + 150 + 500 – 80 – 20

= 650

So the total operational value of the firm is 650.

Does this mean, that if somebody were to buy only the operational assets and liabilities of this Firm, would he have to pay 650?

Well not actually.

In a Balance Sheet of a company, all the values are in book value terms.

That is, it reflects the value of each asset and liability at its original cost rather than the current market value.

So in book value terms, the operational value of the Firm is 650.

But if somebody were to BUY it, we need to find the Market Price of the Operational Value of the firm.

This market price of the operational value of the firm is called ENTERPRISE VALUE.

So how can you arrive at the Enterprise value of the Firm?

To do this, we have well established scientific methodologies like The Discounted Cash Flow (DCF) valuation which is very frequently used.

We can calculate the Free Cash Flows to Firm (FCFF) and discount it using the Weighted Average Cost of Capital (WACC).

So Enterprise value is simply the market price of the all the operational assets and liabilities of a Firm.

Lets say the Enterprise value of the above company comes to 1000 using the DCF approach.

Equity value

The equity value is a straight forward value.

It represents the market value of the share-holders’ capital that is invested in the business.

That is, how much would somebody have to pay to buy the EQUITY ownership of the Firm.

When somebody buys EQUITY ownership of a Firm, he is entitled to both operational and financing assets and liabilities of the Firm.

In other words, he is BUYING the whole Firm.

In our above example, the book value of Equity is straight forward.

It is given as

Total assets – Total liabilities

= Cash + Inventory + A/R + Plant and Machinery + Investments – A/P – IT payable – ST Debt – LT Debt

= Operating book value + Cash + Investments – ST debt – LT debt

= 650 + 50 +100 – 100 – 400

= 300

So the book value of equity comes to 300 which is also what we have on the Balance Sheet.

It matches.

So how do we then calculate the market value of equity.

Well, in the above formula, we can simply replace the Operating book value with its market value.

So we can write the market value of equity as,

Enterprise value + Cash + Investments – ST debt – LT debt

In our above example, it becomes

= 1000 + 50 + 100 – 100 – 400

= 650

So the Equity value comes out to be 650.

As you can see, Enterprise value and Equity value both reflect very different things.

We should be careful not to use them synonymously.

For valuing a company, we first calculate the Enterprise value and then derive the Equity value.

This was clear, isn't it?

Interested in learning how to carry out the valuation of a real company? Check out our Company Valuation and Financial modeling online course here.

Please log in to provide your comments!